Vietnam retail pie: sweet but hard to get

By Trang Le, Head of Research & Consultancy, Vietnam, JLL

Vietnam, 15 Jan 2020 – Vietnam is currently one of the most dynamic economies in the region, bringing with it the development potential for a still young retail market. Trang Le, Head of Research and Consulting Services, JLL Vietnam shows an insight into a market which has been growing more attractive but also competitive for foreign investors.

Demographic and macroeconomic data shows that Vietnam is in the golden phase for economic development in general and retail in particular. The country is forecast to produce the highest GDP growth rate in the dynamic Southeast Asia region with 6.6 per cent, far outpacing the 5 per cent annual growth of the region in the next decade.

Urbanisation is one of the main factors driving Vietnam's GDP growth. Vietnam's urban population is expected to increase at a 2.6 per cent compound annual growth rate (CAGR) until 2030, the highest in Southeast Asia. 36 per cent of the Vietnamese population lived in cities in 2018, compared to 55 per cent and 60 per cent in Indonesia and China.

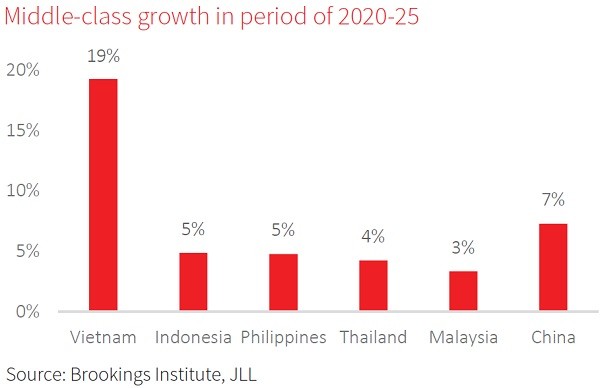

As more people move into cities and take on higher-value manufacturing and service jobs, their incomes also increase. According to data from Brookings Institution, Vietnam is expected to have the highest middle-class population growth in the region, at 19 per cent CAGR in 2020-2025. This is much higher than the 14 per cent recorded in the past decade and higher than the projected regional average of 11 per cent.

Demographics are also a favourable factor in the Vietnamese market. With 90 million people, Vietnam is attracting retailers with its relatively young population with 70% between the ages of 15 and 64 – promising to be a key driver of strong market growth.

Other factors such as the growth of tourism also helps bring more demand for retail. The development of infrastructure also provides investors with more opportunities to develop retail projects outside the central areas.

Potentials and challenges

The potential of the Vietnamese retail market has attracted the attention of many regional mall investors as well as retail investors in the region. Since 2014, the market has witnessed a series of mergers and acquisitions (M&A) deals. An example is Berli Jucker’s acquisition of Metro Cash & Carry Vietnam, the largest M&A deal ever in Vietnam. Shortly after, Central Group – another Thai giant – acquired Nguyen Kim Trading JSC, Vietnam's leading electronics retailer, and Big C Vietnam, the second-largest supermarket chain in terms of the number of stores in the country. E-mart – South Korea's leading retailer – also officially joined the playground in 2015 with a $60 million shopping mall in the north of Ho Chi Minh City. Also from Korea, Lotte Mart has been quite successful with a series of supermarkets and shopping centres across the country. AEON, one of the world's leading retail groups from Japan, is also gradually expanding its network with a fifth centre in Hadong, Hanoi, going into operation in November 2019. Also from Japan, Takashimaya has been present in Vietnam since 2016 at a prime location in the heart of Ho Chi Minh City.

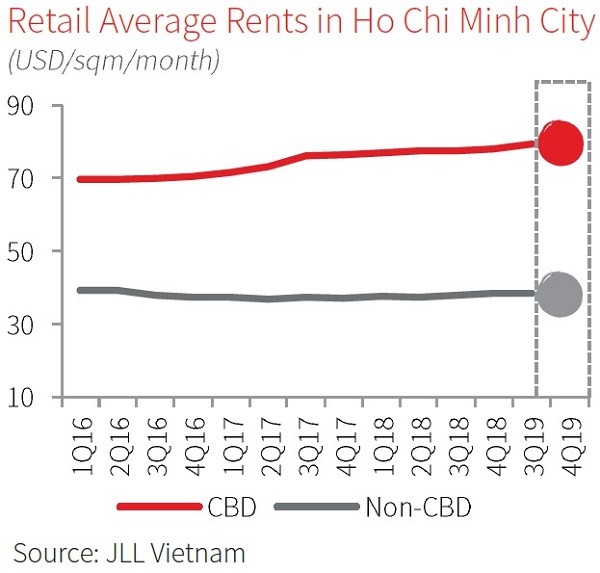

Good rental demand has made prospects brighter for shopping centres, especially projects in the Central Business Districts (CBD). In the third quarter of 2019, occupied space remained stable at about 90% CAGR in both the CBD and non-CBD areas. The market is currently seeing tenants looking for properties with more than 1,000 square metres, making it difficult to find a suitable location at the current retail centres. Most tenants are thus waiting for future supply or retail centres that are currently undergoing renovation and upgrade. Rents at the centres remain stable. A prime location in the CBD is still the most preferred choice for retailers, thus recording the highest price and good growth.

However, retail is still no walk in the park and players are being knocked out left and right by the fierce competition. This is evident in the withdrawal of big brands like Auchan, the shrinking domestic network of Parkson, and the series of foreign convenience store brands struggling to gain market share or having to transfer to domestic rivals (Shop and Go being prime examples).

Lessons and directions for the future

The ups and downs of popular brands in the market tell of the potential of the local retail market – but also show that the apples are not just for anyone to pick.

In addition to the prerequisite of choosing a location with high population density and strong purchasing power, changes in consumer habits, as well as competition from e-commerce, led to the development of new retail models. Retailing in accordance with the target market is the factor deciding a brand's success or failure.

AEON’s success with its "slow and steady" market entry strategy shows that it is extremely important to understand consumer behaviors and select the right retail model. Having a representative office in Vietnam since 2008, it was not until 2014 that AEON officially opened its first centre, Aeon Mall Tan Phu Celadon (Ho Chi Minh City). Choosing the right model that offers a prime spot for families to shop and play in line with the market trends has brought this brand a great deal of success in its five years of operation.

However, for every success, there are multiple instances of failure. Parkson’s less diversified tenant structure which focuses too much on fashion and cosmetics while neglecting dining and entertainment or Auchan and Shop & Go’s disappearance fom the market all profess to the dire need to align with market trends.

In addition to independent shopping centre projects, the market also has a significant supply of retail space from commercial podiums in apartment buildings. This type of retail real estate is struggling to find a suitable direction and model due to its limitations in scope, concept, inexperienced developers, and high competition. According to JLL, at this type of retail real estate, investors should focus on providing utilities for residents first. In addition, other models such as shared office space (flexspace), education systems, or even smart lockers should be considered.

To succeed, retail operators need to conduct careful studies to better understand the trends that will shape the retail market. According to JLL's observations, in addition to the tendency to focus on food and beverage as well as entertainment to increase traffic, developing green retail space, the application of technology and big data, setting up omni-channel shopping, and other creative efforts to enhance the shopping experience will also become more pronounced in the retail market.

In the face of changing shopping behavior and intense competition from e-commerce, "experience" and the "right model" will be the key words for the success of traditional physical shopping and real estate properties.

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $16.3 billion, operations in over 80 countries and a global workforce of more than 93,000 as of September 30, 2019. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.