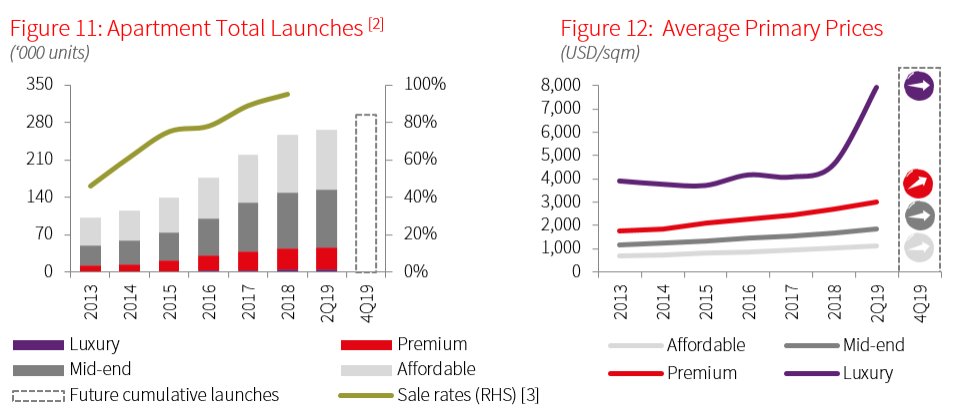

2Q19: Demand for apartments remains healthy as the supply falls sharply in HCMC and Hanoi

Official launches reached more than 4,100 units, the lowest level since the market bound back in 2014, due to the continued prolonged construction approval process experienced recently

VIETNAM, 5 July 2019 – The ratio between the numbers of booking available stock was up to 3:1 for town house and shophouse products at a price range of USD 170,000–USD 250,000 per unit. Demand remained high, stemming from both owner-occupiers and buy-to-let investors.

Most new supply comes from subsequent phases of existing projects. New launches totalled 632 units, mainly from the following phases of Simcity, Van Phuc City and the City Land Park Hill projects. Most new supply targeted town house and shophouse products, while the stock of new villas was limited.

Similar to the apartment market, limited new supply in the RBL property market was mainly attributed to the deferred procedure in granting developers the necessary legal documents to launch projects as planned.

The primary price in 2Q19 escalated to USD 4,198 per sqm of land, up 18.7% y-o-y. This high growth rate mostly came from the record high prices in the new supply of town house and shophouse product types located in established residential areas. The average primary price for villas was recorded at USD 3,729 per sqm of land, remaining stable q-o-q on a project basis. The Villa chain-linked price growth recorded a good rate of 17.0% y-o-y.

Outlook

Similar to the apartment market, the projected number of launches during the year varies widely due to the unpredictable timeline relating to legal procedures. New launches of RBL property are expected to reach 2,200-3,300 units in 2019, 29.0% lower compared to the forecast number in 1Q19.

Given the strong sentiment, most existing projects are expected to improve their prices, especially for Low to Mid-end RBL projects.

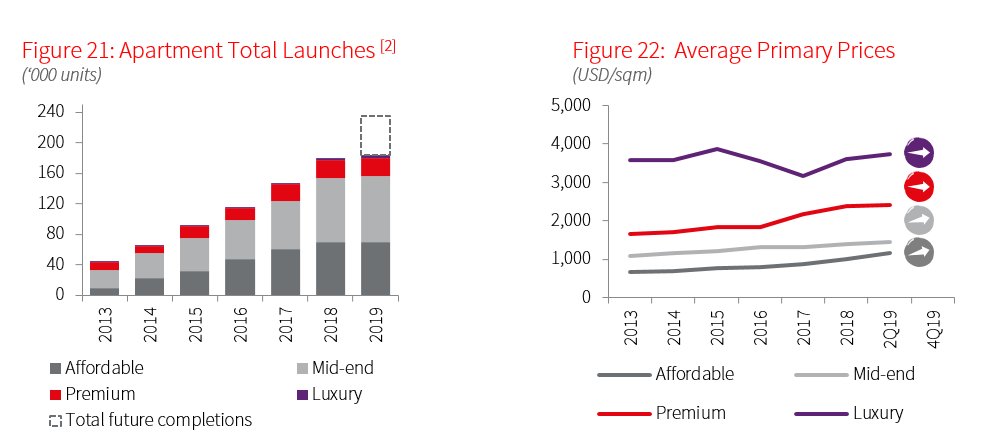

On Hanoi market, after a period of strong influx of stock, 2Q19 registered only 5,900 units newly added to the market, nearly half the 1Q19 figure. Of that, most came from the subsequent phases of existing projects. This was also the lowest level of new launches since the market rebounded in 2014. The majority of new launch projects are small scale with less than 500 units per project.

Unfavourable market sentiment owing to the tightening loan assessment process has prompted developers to introduce more sales incentives schemes to offload stocks while keeping the price unchanged. Most applied sales strategies that included extended payment periods and discount programmes from 3 – 6% on unit price for early payment.

Take-up in 2Q19 was more than 4,660 units, notably lower by 65.3% q-o-q, in tandem with the supply slump. In 2Q19, the slower investor demand became more evident after a period of strong growth. While the demand from owner-occupiers has remained healthy, the widespread trend of increasing interest rate and a stricter loan assessment process among commercial banks have prevented buyers in accessing the mortgages.

Download Vietnam Property Market Brief 2Q19 Here.

>>Read more about JLL Services

>>Read more about JLL News

>>Read more about JLL Research

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $16.3 billion, operations in over 80 countries and a global workforce of over 91,000 as of March 31, 2019. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.