Foreign Direct Investment (FDI) – 10 years’ reflection and real estate development

By Khanh Nguyen, Associate Director, Capital Markets of Vietnam, JLL

|

HO CHI MINH CITY, 7 Aug 2018 – Over the past 10 years, despite the ups and downs of Vietnam's economy in general and the real estate market in particular, FDI inflows remained stable with the cumulative total registered FDI reached the level of approximately US$318.72 billion by the end of 2017, in which cumulative direct investment in the real estate sector achieved US$53.2 billion, according to FIA's statistics. |

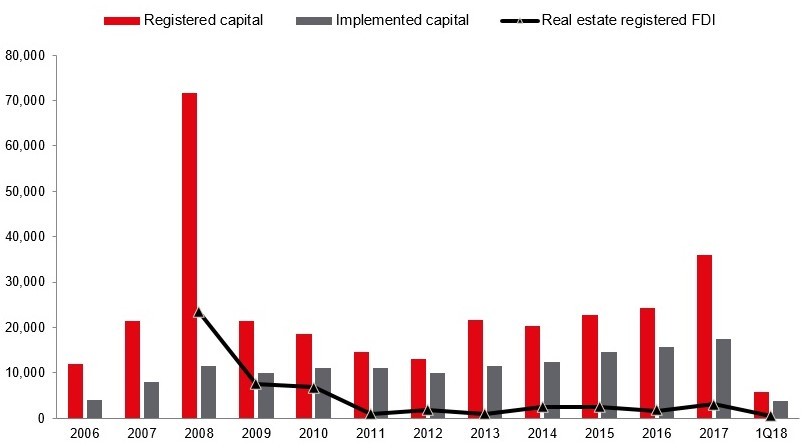

Most notably, FDI into Vietnam in the recent 3 years (2015-17) has continuously increased as compared to the period of 2010-13 and most of the capital inflow was deployed into projects. In contrast, capital inflows to Vietnam in 2007 was triple that of 2005, and peaked in 2008 with the registered amount of almost US$72billion, as capital inflows almost quadrupled in a year (Figure 1). It is important to note that most of the capital was not deployed into projects during that time. While capital inflow in 2008 was six times higher than 2005, the number of projects implemented was just 10% higher in 2008 compared to 2005. However, this amount was never fully disbursed. The FDI in the recent years is to attract realistic projects that will disburse their commitment rather than holding while attracting co-investors.

Figure 1: FDI's by year (US$ million)

Source: GSO, FIA

1Cumulative registered FDI is the successive additions of registered investment from effective projects only up until 20th December 2017.

FDI inflow into Vietnam real estate market

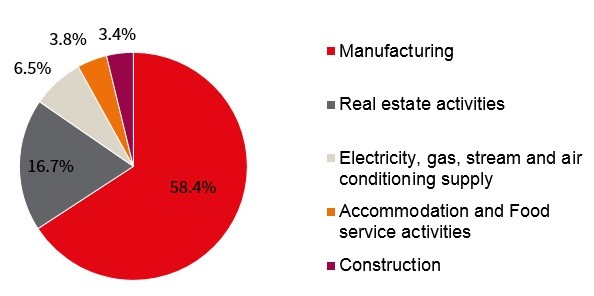

Over the years, FDI inflows into the real estate sector in Vietnam have often been ranked second or third, followed by manufacturing – the largest recipient of FDI among Vietnam's sectors. (Figure 2).

Figure 2: Top 5 Vietnam's FDI by economic activity

Source: FIA Vietnam

(*) Cumulative to 20/12/2017 - Effective projects only

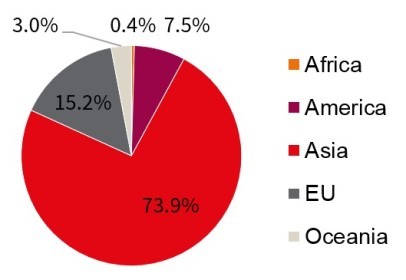

Vietnam's strong and stable growth performance over the past decade has been an attractive magnet for foreign investors, especially those from Asia such as Japan, Korea, Singapore, Hong Kong, Taiwan and China. Their market share accounted for 73.9% of total FDI of all industries including real estate, followed by the EU countries at 15.2% (Figure 3). Most of EU investors invest in the fields such as design, electronics, home appliances and furniture, etc. However, with the need to expand their footprint to Vietnam, these European firms also have increasing demand for direct investment in commercial real estate through acquiring buildings for their headquarters or showrooms in non-CBD areas.

American investors are also key players in Vietnamese market as they ranked third in FDI capital. Although there are no official break-down statistics on FDI inflows into real estate sector by countries, it can be seen that there has been increasing interest from private equity firms in real estate market as they consider Vietnam to be an attractive investment destination. One of the notable American investors is the New York-based private equity firm Warburg Pincus, who has committed over US$1 billion in Vietnam, in which a majority of this fund is allocated to set up real estate platforms including retail, hotels, industrial and logistics.

Figure 3: Breakdown of Vietnam's FDI by region (*)

Source: FIA Vietnam

(*) Foreign direct invested capital till valid as of 20 Dec.2017

FDI of all economic activities including real estates. FDI from the EU is ranked second following Asia.

High-end residential market – the top choice of foreign investors

As more than 10 years ago, FDI inflows were concentrated in the high-end residential segment. Famous names in the market such as Keppel Land, CapitaLand with the first high-end real estate projects in Vietnam such as The Estella or The Vista. With the total supply of high-end apartments in HCMC as of 4Q2007 at approximately 1,700 units, of which about 1,000 units were from FDI projects, it is clear that this is a very small proportion compared to the total population of 6.85 million people in the same year.

Since the market share of FDI projects is not high, the average price of high-end primary stocks in 2007 was at US$2,800/sqm (exchange rate 16,112 VND/US$), representing an increase of 86% as compared to the sales launch of the previous year. This created a virtual supply-demand imbalance that pushed prices beyond affordability of home buyers with real demand. There has been a long queue of buyers trying to compete for a very limited availability of these products due to virtual speculation. During this period, the expected return of real estate investment projects by foreign investors is usually at 30% - 35%, which is very high and attractive for real estate projects, leading to the status of registered FDI on real estate investment, mainly from the Asian countries, reached a record high in 2008, up to US$23 billion, accounting for more than 30% FDI registered capital. (In the last three years, this rate is maintained at 7% -9%).

Until March 2008, with the overheating of the market in 2007 and the impact of the global financial crisis, monetary instruments were unmanageable as interest rates increased rapidly which reached 25% and peak inflation at 23%. Subsequently, the real estate market fell into a recession and FDI inflows to real estate sector also decreased. This capital flow started to recover by the end of 2013, early 2014.

Since then, the market has become more familiar with the names of other FDI investors such as Hong Kong Land (The Nassim project), Frasers Property (Q2 Thao Dien project) or Mapletree (One Verandah project). JLL also noted that they are not new investors in the Vietnamese market, but rather looking to expand their residential portfolio outside of traditional investment in the construction / ownership of leading Grade A or Grade B office buildings in Hanoi (Pacific Place, Central Building, 63 Ly Thai To) or in HCMC such as M Plaza and Me Linh Point Tower. In addition, there are other prestigious investors from Japan such as Daiwa House, Nomura and Sumitomo to invest in projects in District 7 or Korean corporations such as Lotte Group, GS Investments in Thu Thiem New Urban Area in District 2.

Emerging trend to expand FDI inflows into the mid-end and affordable housing segments

With the recovery of the real estate market, foreign investors, especially those from Japan, are looking to pour their capital into Vietnamese real estate market. This is proven by the deals announced in the past three years by Japanese investors such as Hankyu Realty and Nishi Nippon Railroad in cooperation with Nam Long or Sanyo Homes and Tien Phat, and most recently the joint venture between Mitsubishi Corporation and Phuc Khang. Investment segment of diversified joint ventures are targeting the mid-end and affordable segment. Following this trend, there are many investors considering and willing to participate in joint ventures and contribute capital with reputable Vietnamese investors. The advantages of such joint ventures are that the Vietnamese local investors can contribute their understanding and knowledge of the market, the legal system, the established list of real estate portfolio while foreign investors with strong financial capacity and real estate project development expertise will add more value to the project.

And commercial real estate with FDI also gradually increases supply over the years

With the total office supply 10 years ago was about 650,000 m2, until now, this number has increased by three times, of which, the supply from office buildings with FDI contributions increased to 500,000 m2, doubled since the past 10 years. Previously, with the demand for Grade A office space, tenants have only a handful of options from Grade A buildings built since the 90s, such as Sunwah Tower, Diamond Plaza, Saigon Center (Phase 1) or Metropolitan. Over the past five years, the market has witnessed a significant increase in Grade A supply from FDI investors such as Vietcombank Tower, Saigon Center (Phase 2) and Deutsches Haus. Not only the traditional office business, the office market embraces a diversity of new investment concepts such as co-working spaces or serviced offices. We expect the trend to accelerate, due to (1) changing demographics and working styles; (2) companies realizing the need for flexibility in their leases due to rapid changes in business environment.

Real estate FDI prospects for 2018

2018 marks a 10-year period since the downturn of the real estate market and nearly 5 years of market recovery. Given the monetary policies are expected to stay neutral-to-accommodative to support growth when FDI inflows in hundred millions of dollars are poised to enter the real estate market in Vietnam, we expect the real estate market to continue stabilising and growing. M&A activities and other forms of direct investment will continue to reach new records.

- We forecast the real estate market outlook as following:

- Deals are available but harder to execute due to divergence in pricing expectations between buyers and sellers.

- More opportunistic funds will focus on new areas (e.g. school, hospital, construction).

- Limited yield compression but asset prices should rise further due to rent growth.

- Demand for co-working space is growing from both small and large enterprises.

- REITs to expand capital sources. By the end of 2017, the notable transactions of Pullman Jakarta Central Park Hotel in Indonesia, Capri by Frasers HCMC and IBIS HCMC in Ho Chi Minh City with total investment portfolio value of US$130 million by a Thai-listed REIT (SHREIT) have proven the intra-regional capital flows and the appeal of investment assets in Vietnam to international investors.

- Continued strong interest in industrial and logistics assets. The lack of high specification, modern logistics warehouse space and strong demand from regional occupiers are supporting for the potential growth of this industry. As such, this sector remains on the radar of foreign investors and developers in 2018.

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $16.3 billion, operations in over 80 countries and a global workforce of over 91,000 as of March 31, 2019. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.