4Q19: Strong demand for mid-end apartments

Sustained demand continued, yet 4Q19 sales only halved of those in 4Q18 , mainly due to limited supply caused by ongoing restricted approval procedures.

Ho Chi Minh City

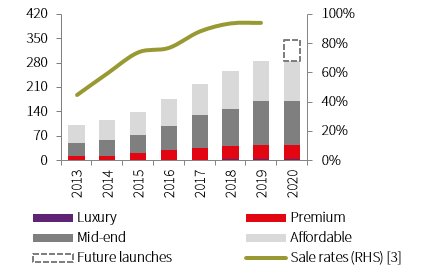

For the entirety of 2019, sales totalled more than 30,000 units, albeit 35% lower than the peak year of 2017, still 5-6 times more than 2012-13 downturn period.

Mid-end projects with a launching price of USD 1,200-USD 1,700 per sqm remained the top performers, accounting for 70% of units sold in 2019 as they were situated in good locations, offered a wide range of amenities, while still had large room for price increase, attractive to both owner-occupiers and investors.

After an exceptional quarter with more than 10,000 units from the Rainbow phase of Vinhomes Grand Park project launched, the market returned to quiet mode with only 3,600 units officially launched in 4Q19, a result of the prolonged approval process. For the whole 2019, official launches[2] totalled nearly 30,000 units, which was 20% below 2018’s number and 30% below the peak year of 2017.

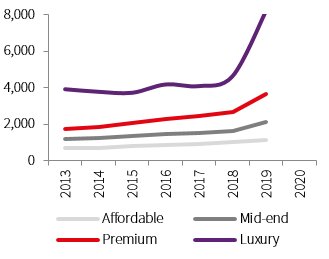

In 4Q19, the average price reached a record high of nearly USD 2,900 per sqm, up 78.2% y-o-y and 39.8% q-o-q. This exceptional improvement in price was mostly driven by i) most projects with lower prices were sold out, the basket was therefore left with those with higher-than-average price; and ii) developers having projects launched in the quarter had more confidence in pricing given the tight supply. Meanwhile, the chain-linked rise by 22.9% y-o-y and 1.7% q-o-q, driven by sustained demand.

About 30,000-35,000 units are expected to launched officially in 2020, mainly contributed by Vinhomes Grand Park project. It should be noted that the number is subject to a great deal of uncertainty given the government’s tight control in granting land use rights and construction licences. Strong demand is set to carry on and will boost the price further across all sectors. However, the demand in high-end segment, especially from investors, is likely to slow down in long term as their already-high price level and low rental yield make it a less attractive investment.

Figure 11: Apartment Total Launches

“000 units

Figure 18: Average Primary Prices

USD/ sqm

Ha Noi

In 4Q19, take-up totalled 7,429 units, still at high level though observed decrease q-o-q due to the year end holiday season. Although sales eased through the quarter, number of unsold units remained low at end-2019 amid limited supply, down 18% y-o-y.

It should be noted that buying sentiment towards newly launched projects remained upbeat in the quarter, with Vinhomes Symphony in Long Bien District and Mipec Rubik 360 in Cau Giay District able to sell over 90% and 70% of the launching units within one week, respectively. Other than that, pre-sales rate of some new projects is increasingly supported by foreign buyers as local developers had ramped up their overseas marketing efforts.

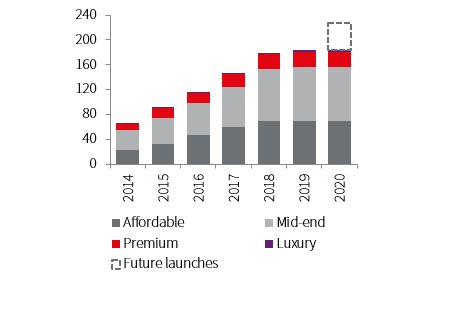

Over 7,740 units were launched in 4Q19, down by 8.2% y-o-y. In 2019, new launches totaled around 32,060 units, predominantly attributed to the mid-end apartments with 75% market share. The recently announced land base price policy to increase next year has likely prompted developers to delay new launches with the view of higher selling price of their properties in 2020.

Residential market remained the most active sector in terms of investment enquiries. Foreign development groups from across region particularly Japan, Korea and China continued to explore the development opportunities in prime locations as well as in surrounding neighborhoods.

The average price level stood at USD 1,501 per sqm, grew moderately 1.5 % q-o-q. Mid-end segment was the best performer thanks to entrance of some new projects in good location and developed by reputable developers. Notably, the quarter witnessed one luxury project return to the market after a long delay with a soft – launching price at USD 6,000 – 8,000 per sqm, an exceptional high price recorded in the city west area.

The residential market in 2020 is expected to see an influx of luxury apartments . An estimated 1,000 luxury units from four projects are set to be launched next year, accounting for nearly one third of the total existing luxury stock. Expected heightening prices combined with positive economic outlook will likely prompt buyers to rush to the market, thereby supporting transaction volumes.

Figure 21: Apartment Total Launches

“000 units

Figure 22: Average Primary Prices

USD/ sqm

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $16.3 billion, operations in over 80 countries and a global workforce of more than 93,000 as of September 30, 2019. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.