JLL: Overview HCMC and Hanoi Retail 3Q 2018

In 3Q18, Vincom Center Landmark 81 officially opened, providing over 46,000sqm GFA to HCMC retail market.

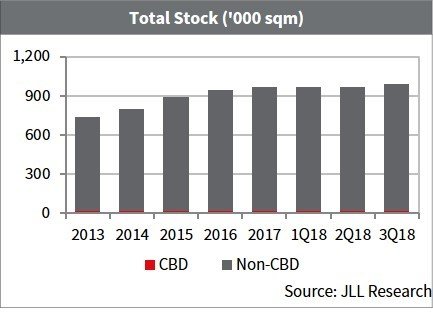

Supply increased in non-cbd: In 3Q18, Vincom Center Landmark 81 officially opened, providing over 46,000sqm GFA to HCMC retail market. Besides, a shopping mall in non-CBD sub-market was converted into other function. Accordingly, as end of 3Q18, the total stock reached 989,400sqm, increased 2.8% q-o-q and 15.3% y-o-y.

Demand remained positive: The decrease of 204bps q-o-q in occupancy rate was attributed to the entrance of the new supply and the restructuring of the tenant mix in a big shopping mall in non-CBD area. F&B and entertainment tenants continued to show good performance and were the most active group of tenants in the city.

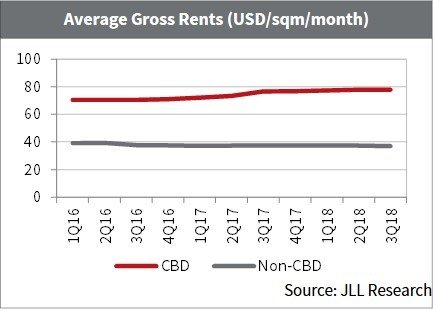

Rents decreased slightly: The overall market rent was at around USD46.2 per sqm per month, slightly decreased by 0.2% q-o-q and 0.7% y-o-y. In non-CBD sub-market, a department store was reoriented both its business concept and pricing strategy, targeting lower market segment. As a result, the average rent of this sub-market reduced by 0.4% q-o-q to USD37 per sqm per month.

Outlook

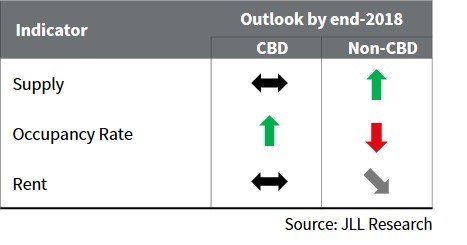

Enrichment in future supply: By end-2018, the market is expected to welcome more new supply, focusing in non-CBD area such as Estella Place (District 2), Cong Hoa Garden (Tan Binh). In spite of the forceful growth of e-commerce, market performance of retail market in HCMC has not recorded significant impact. Yet, in order to catch this emerging trend, future supply should be developed as a destination, providing entertainment, showroom and lifestyle experience for a diverse group of customers rather than a purely physical shopping place.

CBD continue to attract more tenants: More foreign retailers are set to enter the market, especially in CBD sub-market where the occupancy rate and rental rate likely continue the upward trend. Meanwhile, non-CBD sub-market is likely to witness the surplus in supply in the coming quarters.

[1]: Shopping centre/Department store

[2]: Gross rent includes service charges/management fees but exclusive of VAT.

[3]: Average gross rent, q-o-q and y-o-y changes are adjusted to remove the effects of supply additions/removals (i.e. changes are on a like-for-like basis).

HANOI RETAIL

Supply increase: There was no new prime retail space in 3Q18. Approximately 24,000 sqm of shopping centre space opened in the non-CBD area in 3Q18, pushing the total retail stock to more than 987,000 sqm. Convenience stores remained robust growth during the reviewed quarter, with total existing of nearly 75,000 sqm, mostly attributed to favourable retailers and recent new entrants, such as Co.op Food.

Healthy demand: Quarterly total net absorption was approximately 66,000 sqm, mainly driven by the new supply in the non-CBD sub-market. The new shopping centre achieved high occupancy rate of nearly 80% when opening.

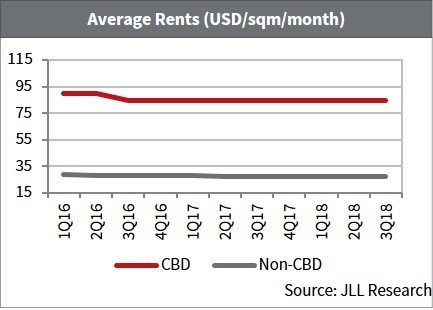

A modest decrease in rent: The average rent of SC/DS saw a slight decline of 0.4% q-o-q. In 3Q18, shopping centre in the CBD remained unchanged at USD 100 per sqm per month, while the non-CBD properties witnessed a mild fall to USD 27.3 per sqm per month, down by 0.4 q-o-q. The rental growth of prime retail space in 3Q18 was 0.9% q-o-q, thanks to the high demand and restricted supply.

Outlook

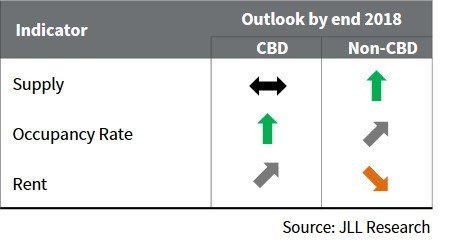

More supply in CBD-fringe submarket: More than 96,000 sqm is expected to be opened by the end of 2018, 52% of the total high-quality retail supply located in CBD-fringe area.

Rent to decline slightly: Abundant supply in the pipeline along will put downward pressure on Hanoi retail rent in CBD-fringe submarket over the next two years. Several non-CBD shopping centres are likely lower their rents and restructure the tenant mix and layout to boost the footfall.

[1]: Shopping centre/Department store

[2]: Gross rent includes service charges/management fees but exclusive of VAT.

[3]: Average gross rent, q-o-q and y-o-y changes are adjusted to remove the effects of supply additions/removals (i.e. changes are on a like-for-like basis).

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $16.3 billion, operations in over 80 countries and a global workforce of over 91,000 as of March 31, 2019. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.