Southeast Asia’s office demand seen rising 6% annually in the next four years

As Southeast Asian economies expand, office demand, particularly from technology, e-commerce and coworking companies, is expected to rise by an estimated 6% annually between 2018 and 2021.

HO CHI MINH CITY, 28 Aug 2018 – As Southeast Asian economies expand, office demand, particularly from technology, e-commerce and coworking companies, is expected to rise by an estimated 6% annually between 2018 and 2021.

Based on JLL's latest outlook report for the second half of this year "Southeast Asia set for further outperformance," office take-up in the region accelerated over the last six quarters as demand continued to surprise on the upside, notably in Manila, Singapore and Jakarta.

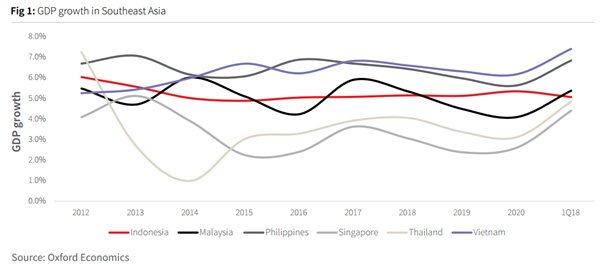

"Technology, e-commerce and flexible space operators were key demand drivers," says Regina Lim, Head of Capital Markets Research, Southeast Asia. "Looking forward to 2018-2022, we expect office take-up in Southeast Asia to stay strong, growing at 6% annually, amid GDP growth of 5% per annum", she said.

According to the report, accelerating economic growth, government initiatives such as Thailand's Eastern Economic Corridor, strong tourist arrivals and continued expansions by e-commerce and co-working operators will support demand for commercial real estate going forward. However, upcoming elections in Indonesia and Thailand in 2019 may cause short-term uncertainty.

The report highlighted some of the key trends in each market:

Ho Chi Minh City and Hanoi expects high demand

As end of 2Q18, the total stock of HCMC office market increased to 1,945,000 sqm with the overall Grade A and Grade B occupancy rate standing at the high level of above 95%. The overall rental rate is expected to continue the upward trend with support by healthy demand and increased quality in future supply. A large volume of high-quality Grade B supply is also projected to complete by 2020 and will likely put pressure on Grade A sub-market in the future, especially long-standing Grade A projects with the degenerated construction quality.

In Hanoi, demand for Grade A & B office in 2018-2019 will increase on the back of positive economic growth. Higher occupancy rates were observed in both Grade A and Grade B office market as new set-up and relocation purposes continue to be the main drivers of office demand.

Stephen Wyatt, Country Head of Vietnam, JLL comments:" Vietnam is considered to be one of the fastest growing e-commerce and flexible space markets in the region. This uprising trend will have a positive impact on the office market as companies, both foreign and local, will be looking for a suitable place to set up operations in this promising economy."

Singapore office rent forecast to rise

Singapore prime office rents started to recover in the first half of last year and are forecast to rise 20-25% over the 2018-2020 period, the fastest pace of growth amongst global cities. In the first six months of this year, JLL upgraded Singapore CBD Grade A office rents and capital values for 2019 marginally as some aging stock may be withdrawn for retrofitting and redevelopment, boosting occupancy rates. The property consultancy also expects prime retail rent to climb between 0.5% and 1% for the next four years.

Jakarta's absorption to stay strong

While 2018 is expected to be another record year for supply, net absorption is expected to stay extremely strong as technology, coworking and other CBD tenants continue to expand. JLL expects rents to fall another 2-3% in the second half of the year before recovering gradually from 2019.

Kuala Lumpur's fringe areas to outperform

While office rent in Kuala Lumpur (KL)'s city takes longer to recover due to a significant volume of new supply, JLL expects the fringe areas to perform better with limited supply coming on stream and strong demand due to its excellent connectivity. JLL downgraded its prime office rent and capital value forecasts for KL City by 2.3% and 6.0% respectively; and raised its forecast for KL Fringe by 2.6% and 0.6% respectively.

Stronger-than-expected demand in Manila

The biggest upside surprise in 2Q18 was the strong office take-up in Manila, where net absorption increased by 222,000 sqm (Net Lease Area) in 2Q18, with strong demand from Outsourcing and Offshoring companies, online gaming operators and business services firms in travel, marketing and IT. Despite the record volume of office completions in 2018, the vacancy rate has stayed at 2.2% in 2Q18 as the take-up of the new buildings was stronger than expected. JLL has revised the vacancy rate forecast with occupancy now expecting to stay above 96% by 4Q18, compared to our previous estimate of 94.7%.

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. Our vision is to reimagine the world of real estate, creating rewarding opportunities and amazing spaces where people can achieve their ambitions. In doing so, we will build a better tomorrow for our clients, our people and our communities. JLL is a Fortune 500 company with annual revenue of $16.3 billion, operations in over 80 countries and a global workforce of over 91,000 as of March 31, 2019. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.com.