Flexible space makes economic sense in Asia Pacific

Flexible space remains popular among start-ups and small firms. But now even corporate occupiers are increasingly incorporating it into their Asia Pacific leasing strategies.

Unit economics is a key consideration when occupiers choose between a flexible and conventional space. Both options can make economic sense for large requirements depending on an occupier’s real estate strategy, size and time horizon.

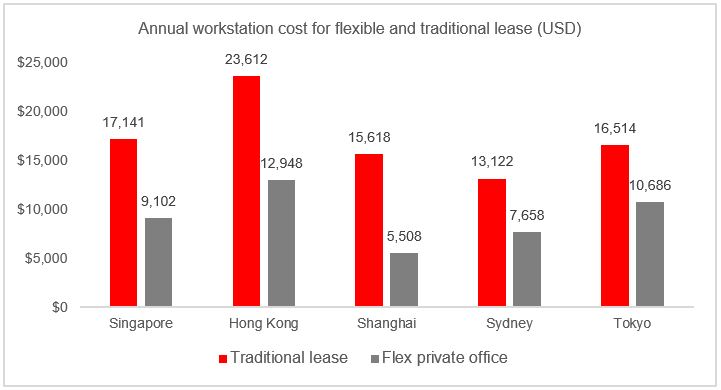

Chart 1: Flexible space is less expensive on a workstation basis in key Asia Pacific markets

Source: JLL Research, 2019

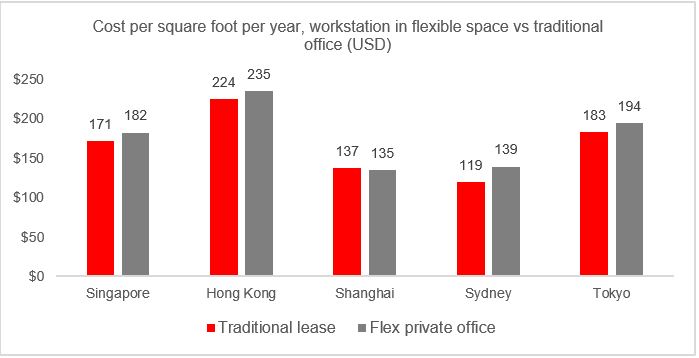

Chart 2: But conventional office space is more cost effective on a floor area basis

Source: JLL Research, 2019

Recently, JLL research compared occupancy costs of both flexible space and a conventional lease, across major Asia Pacific markets. Not surprisingly, we found that conventional leases are almost always cheaper on a floor area (per square foot) basis, whilst flexible space is cheaper on a workstation basis. After all, a high density of workstations is part of the flexible space business model.

But does flexible space always make economic sense? The research compared the cost of both types of spaces and their breakeven points under three common scenarios: 10 workstations, 50 workstations, and 200 workstations.

It revealed that the economics of flexible space is compelling for all requirements for tenures up to about three years. It is even more compelling for occupiers requiring up to 50 workstations. For example, if an occupier takes 10 workstations, the total cost for flexible space will always be cheaper than a conventional office, even if premium pay-per-use services are charged on top of the rent. In such cases, it will make little sense for occupiers to opt for a conventional lease, as their requirements are less. They would rather reinvest in their growing business than go for capital expenditure.

Additionally, flexible space offers agility to fast-growing businesses. For now, occupiers who take up smaller numbers of workstations are typically start-ups. It also gives them access to central locations that they may not be able to avail otherwise.

For occupiers taking some 50 workstations, the flexible space option is economical only up to five years. Beyond that, they can achieve more cost-savings with conventional leases. For occupiers taking up to 200 workstations, the best option is a conventional lease with commitments beyond three years.

In short, flexible space makes economic sense if the occupier has small requirements and short-term needs. Conversely, conventional leases are more economical for larger teams on a long-term basis.

Is cost alone the reason for occupiers opting for flexible space? Recent examples suggest otherwise. There could be different motivations beyond cost. And this is where the trend comes in.

In one unprecedented case, HSBC leased more than 1,000 seats with WeWork in London for an unspecific tenure. That said, while there are many examples of companies of all sizes using a flexible solution (swing space, unanticipated headcount and business need), long-term commitments don’t always make economic sense.

Chart 3: Flexible space is more cost effective than a conventional lease over the near term

Note: JLL examined costs associated with flexible space private offices and conventional office leases in Hong Kong, Shanghai, Singapore, Sydney and Tokyo. Fit-out, reinstatement, office management, utilities, IT infrastructure and running costs were added to conventional office rents to facilitate a like-for-like comparison. Nuances of specific locations and the incentives offered by traditional and flexible space landlords/providers are not captured. Model assumes full occupancy. Key factors affecting cost effectiveness: Fit out/upfront capex, type and volume of space: Hot and fixed desks are cheaper than private offices, workstation density: 5-6 sqm in flexible space and 10-11 sqm for conventional space, and amortization period. Conventional lease workstation allocations are inclusive of common areas, e.g. pantries, and flow through areas.

Source: JLL Research, 2019

How do flexible real estate spaces benefit

investors?