West China’s logistics market development process

Different stages of Grade A warehouse development in Chengdu, Chongqing and Xi’an

Established as the logistics hub in West China, Chengdu, Chongqing, and Xi’an have witnessed a rapid growth of Grade A warehouses over the past ten years. From 2010 to 2015, a batch of foreign logistics developers led by GLP, Goodman, Prologis entered the West China market. At that time, the West was at an early stage of Grade A warehouse development, compared with Jin-Jin-Ji, Yangtze River Delta and Pearl River Delta regions. But an intense arrival of properties over the past five years has reshaped the landscape. It has taken the stock in Chengdu (4.25 million square metres), Chongqing (3.91 million square metres), and Xi’an (3.34 million square metres) to third, fourth and sixth ranking respectively and nation-wide, as of the end of 2020. However, the three cities face many challenges in different stages.

Figure 1: 2015 Q4 vs 2020 Q4 Grade A warehouse total stock in major cities in China

Source: JLL Research

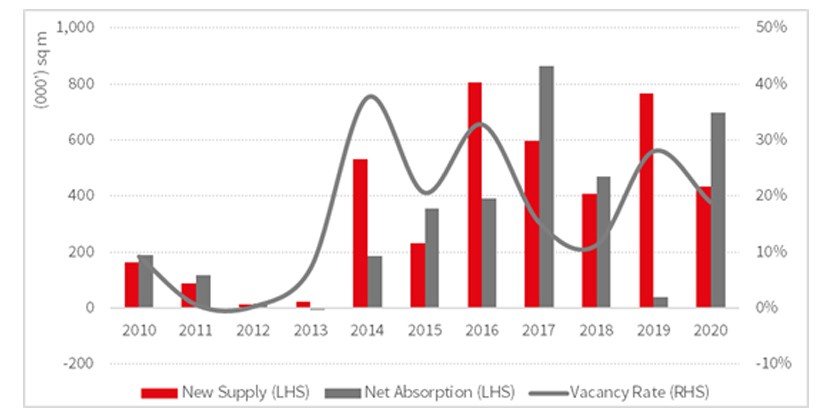

Chengdu: Starting 2019, the Chengdu logistics market has been experiencing the second supply peak. The market has developed new features compared with the first one in 2016. New supply is expected to focus mainly on the Qingbaijiang submarket, making less impact on the overall market, as compared to a city-wide heavy supply in 2016.

On the other hand, the major warehouse demand drivers have changed from e-commerce dominated to more diversified. Changes in the tenant structure contribute to stabilising the demand momentum, reducing the risk of over-relying on the development of a single specific industry. The supply-demand environment has improved since 2016.

Figure 2: Chengdu Grade A warehouse new supply and demand

Source: JLL Research

Chongqing: A strong supply has re-constructed the tenant structure in Chongqing. In 2020, the new supply in Chongqing’s Grade A warehouse hit a record high, 15 projects with a total GFA of 1.17 million square metres completed. Total warehouse stock reached 3.4 million square metres by the year-end. Falling warehouse rent with stronger tenant bargaining power caused by extremely heavy new supply was rewriting the warehouse demand pattern. Many cost-sensitive tenants such as labour-intensive manufacturers and local transport enterprises have upgraded to Grade A warehouses. As a result, the Chongqing logistics market has ushered in a period of popularisation.

Figure 3: Chongqing Grade A warehouse new supply and demand

Source: JLL Research

Xi’an: One of the few logistics markets in West China, it has a balanced supply and demand. Compared with co-located Chengdu and Chongqing, Xi’an is the only regional distribution centre in Northwest China that attracts a large number of e-tailers and 3PLs to set up their RDCs here. The logistics transportation service scope covers most of the Northwest region (including Shanxi, Gansu, Ningxia and Qinghai provinces). In addition, driven by urban renewal and illegal warehouse standardising over the past few years, Xi’an market enjoyed the transition from non-Grade A to Grade A warehouse facilities, stimulating huge upgrading demand. As such, Xi’an warehouse market maintained balanced supply and demand despite a large supply influx in 2018, and the overall vacancy rate stayed below 15% by 2020 end.

Figure 4: Xi’an Grade A warehouse new supply and demand

Source: JLL Research