Vietnam’s Economic Backdrop 3Q21

A positive end to a subdued 3Q

Vietnam recorded the deepest GDP decline in 3Q21 in the history of quarterly GDP statistics since 2000: Vietnam’s GDP decreased 6.17% y-o-y in 3Q21. The only sectors that recorded a positive growth rate were agriculture, forestry and fishery, increasing 1.04% y-o-y. Industry and construction sectors fell by 5.02% y-o-y, while the services sector was down 9.28% y-o-y.

The GDP growth rate in the first nine months only increased 1.42% y-o-y, lower than the last year rate of 2.1%, owing to the adverse impacts of Covid-19, especially in the Southern area.

ADB lowers Vietnam's 2021 growth forecast to 3.8%, down from the 5.8% predicted in July. However, Vietnam General Statistics Office anticipates the economic growth in 2021 to stand at only 2.5%, provided Q421 growth reaches 5.3%. The economic recovery depends heavily on the containment of the pandemic, the roll-out of vaccines and the post-pandemic government policies to support businesses. Despite many challenges, ADB and foreign investors remain upbeat about Vietnam's growth prospects in the medium and long term, with its economy estimated to grow at 6.5% in 2022.

Figure 1: Real GDP Growth (y-o-y)

Total retail sales of consumer goods and services continued to decline significantly, while international tourism continued its downward trend: Due to the serious impact of the pandemic, in the first three quarters of 2021, the total retail sales of consumer goods and services reached VND 3,367.7 trillion, down 7.1% y-o-y. Transportation continued to face difficulties, with 2,018.8 million passengers, down 23.8% y-o-y. In Q321, passenger transportation dropped 69.6% y-o-y as a result of the lockdown. Meanwhile, international tourists arrival to Vietnam was estimated at 114.5 thousand in the first nine months of 2021, down 97% y-o-y.

Figure 2: Retail Sales Growth (YTD) vs International Arrivals Growth (y-o-y)

FDI capital increased positively compared to the same period in 2020 despite the 4th wave of the pandemic: FDI capital reached USD 22.15 billion in the first three quarters of 2021, up by 4.4% compared to the same period in 2020.

Although total FDI increased, its disbursement was down slightly to 3.5% over the same period and stood at USD 13.28 billion.

Among 18 industries attracting FDI, the processing and manufacturing industry topped with USD 11.8 billion, accounting for 53.4% of the total registered capital. It is followed by the utilities industry, with an investment of over USD 5.5 billion, constituting 25% of the total registered capital. Real estate and wholesale & retail are also among the most attractive industries for FDI investment. Regarding FDI partners, Singapore emerged as the largest investor in the first nine months of 2021, with a total of USD 6.3 billion, accounting for 28.4% of the total registered FDI capital, followed by Korean and Japanese investors.

Figure 3: FDI (year-to-date)

Looking for more insights? Never miss an update.

The latest news, insights and opportunities from global commercial real estate markets straight to your inbox.

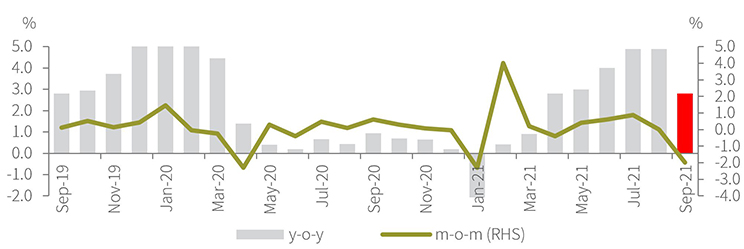

CPI slightly increased: The average CPI in 3Q21 increased 2.51% y-o-y, and the average CPI in the first nine months of 2021 increased by 1.82% compared to the same period in 2020, the lowest increase since 2016.

- The increase in CPI was mainly due to

- the domestic gasoline price increased by 24.8%,

- the education cost increased by 3.76% due to increased tuition fees for the 2020-2021 academic year

- Rates of construction material increased by 6.3% y-o-y due to rising prices of cement, iron, steel and sand and other input costs

- Rice price climbed 6.47% y-o-y owing to the increasing export and the growth in demand due to the lockdown situations.

On the other hand, there are many other reasons for the decrease in CPI in the first nine months of the year:

- The price of food items decreased by 0.29% y-o-y

- Electricity price dropped 0.99% y-o-y since utility charges were cut down in lockdown provinces

- Domestic travelling was restricted due to the pandemic, dragging down air tickets by 20.91% y-o-y

Figure 4: CPI - Overall

Positive growth, however, as of 3Q21, Vietnam had a trade deficit of USD 2.13 billion: Despite the 4th wave of Covid-19, the export value reached USD 240.52 billion, up 18.8% y-o-y, while the import value reached USD 242.65 billion, up 30.5% y-o-y.

The first three quarters of 2021 had an estimated trade deficit of USD 2.13 billion. The US is the largest export partner with a turnover of USD 69.8 billion, up 27.6% y-o-y, followed by China, EU, ASEAN, Korea, and Japan.

As import partners, China is Vietnam's largest market with a turnover of USD 81.3 billion, up 41.1% y-o-y, followed by Korea with USD 40.2 billion, up 21.6% and the ASEAN market with USD 30.7 billion, up 41.2%.

Figure 5: CPI - Housing & Construction Materials

61.4% of manufacturing enterprises were affected in 3Q21, but 43.4% believe that business will improve in 4Q21: Nearly 85.5 thousand new businesses were established in the first three quarters, with a total registered capital of VND 1,195.8 billion and 648.8 thousand registered employees, a 13.6% y-o-y drop in the number of enterprises, down 16.3% y-o-y in the registered capital and 16.6% y-o-y in the number of employees.

The number of enterprises temporarily suspending business increased by 16.7% y-o-y, and those terminating operations and waiting for dissolution increased by 17.4% y-o-y.

In the latest survey by General Statistics Office, 61.4% of manufacturing enterprises admitted to having been facing difficulties. At the same time, 43.4% of enterprises, of which 79.4% are foreign-invested businesses, believed the market would improve in 4Q21.

Figure 6: Merchandise Trade Balance

Looking for more insights? Never miss an update.

The latest news, insights and opportunities from global commercial real estate markets straight to your inbox.

You may also like

What growing cross-border data flows mean for data centres

Uncertainty lingers for Hong Kong’s data centre industry as cross-border data deal unfolds

Southern Industrial Land and Ready-built Factory (RBF) 2Q2022

Land prices continued to rise, whilst RBF rents remained stable

Hanoi Retail Market 2Q2022

Rents increased slightly in the non-CBD area and stabilised in the CBD area